Cash-burning healthcare companies looking to go public may be forced to turn to alternative methods of funding to keep their businesses afloat amid a weak market for initial share sales, industry analysts say.

The IPO market for healthcare tech companies is facing its worst year in two decades as the COVID-19 pandemic, Russia’s war in Ukraine, record-high inflation and rising interest rates have squeezed public market valuations and sent stocks plunging.

Until this year, healthcare technology companies considering share sales had reason to be confident. Public markets soared in 2020 and 2021, spurred by low borrowing costs and pandemic relief funds. A rise in special purpose acquisition companies, or SPACs, meanwhile, helped more private companies reach market.

Last year, 1,035 companies went public on U.S. exchanges, setting a record, according to Stock Analysis. Healthcare companies rode the public market wave, raising a record-breaking $56.36 billion in 403 IPOs.

The fundraising exuberance faded in 2022, however. This year, the number of businesses that have filed to go public has tumbled to 173. Healthcare companies are flagging, too, with only 20 IPO filings as of October this year, excluding SPACs, according to Renaissance Capital.

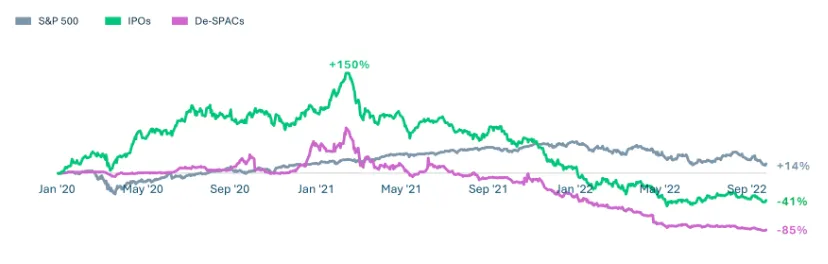

The drop comes as stocks remain down year over year. The majority of healthcare technology stocks were trading negatively as of September with a median performance of -58%, according to investment and analysis firm Silicon Valley Bank.

Experts don’t expect the public markets to quickly recover.

“I think 2023 is gonna be really rough,” said Jonathan Norris, managing director of life science and healthcare practice at Silicon Valley Bank. “I'm hoping that the second half of 2023, you start to see some brighter spots.”

“[There’s] a lot of erosion in public market caps from companies that are long-term public companies as well as recent IPOs over the last few years, and really, that's cast a pall over the ability to get out and IPO,” Norris said. “So the question is ... what are they doing now?”

Capital raising

Companies waiting out a poor public market may turn to private rounds as IPO demand dries up and investors hand out funding more cautiously, analysts said.

Still, relying on private money can carry its own risks. Funding for capital raises has dropped across the board this year. In August, global venture funding declined to the lowest levels in two years.

“Not only are market conditions less than ideal for public exits, but the combination of market downturn, inflation, interest rate hikes, and scrutiny following 2021’s bear market investments have made private capital harder to raise for IPO-stage startups compared to last year,” said Adriana Krasniansky, head of research at digital health venture fund Rock Health.

Healthcare companies specifically have raised less capital compared to 2020 and 2021. The third quarter of 2022 was the lowest for digital health funding for the past 11 quarters, according to Rock Health.

“I've heard a lot of VCs saying that it's prudent to tighten the belt,” said Stephanie Davis, senior research analyst at SVB. “So rather than investing purely for growth, I think a lot of folks are taking a more balanced approach to wait out the storm.”

As overall funding has dropped, companies deciding to raise capital in today’s market may see a drop in their valuations, “aka a down round,” Krasniansky said.

That may lead companies to turn to internal, extension and bridge funding rounds, which could lend companies capital without risking a hit to their valuation, Krasniansky added.

“A lot of these later-stage companies that thought they were all going to IPO couldn't, based on the market conditions, and ended up doing some sort of insider round with their existing investors to try and push out the amount of cash burn as far out as they could and to 2023 or beyond.” SVB’s Norris said. “Basically, that gives them breathing room.”

Healthcare technology companies in particular may be feeling the effects of a negative outlook for the broader tech industry outlook as large companies like Amazon and Meta lay off thousands of workers, said Adam Sorensen, health integration and divestiture leader at EY Americas and strategy and transactions principal.

“The value proposition for, especially, technology-enabled companies in health, is really getting pressure tested,” Sorensen said. “I think it's just going to be harder for them to raise money without a compelling value proposition.”

Companies could pursue other avenues of raising capital rather than equity — like debt and warrants, Davis added.

Due to the stronger funding environment last year, some companies may not need to raise more capital just yet. “There was a lot of fundraising activity that happened at the end of 2021, said Davis. “I don't think you're really going to see a ton of pressure until after the last round of capital runs out.”

Still, those companies may be among the fortunate few, according to Norris.

“There's some [companies] that are just so well capitalized, they have cash into 2024. But I think that's a pretty small percentage,” Norris said, adding that even well-capitalized companies may have to start considering raising funds in the second or third quarter of 2023.

Back to M&A

Capital constraints, depressed valuations and unattractive public market options could drive demand for M&A as companies seek exit options, said Nathan Ray, partner at management consulting company West Monroe.

“I think the demand to bring things to buyers is picking back up,” Ray said. “Those that are buyers are trying to buy and those that need capital are trying to find it or trying to come to the market.”

Although healthcare volume and deal totals have been trending down in 2022 compared to the two prior years, deals may be returning to “new normal” pre-pandemic levels, like 2019, Ray added.

From the sell-side, digital health startups in particular may be more likely to welcome M&A offers that allow them to bolster product, keep down costs and offer liquidity to “impatient investors,” Rock Health’s Krasniansky said.

On the other side, lower valuations could lead strategic buyers to become more opportunistic, said EY’s Sorensen. Although they’re facing a “tougher” environment compared to last year, private equity firms also are continuing to hunt for deals, he added.

“I think there was also just a broader level of interest over the past two years for healthcare technologies,” SVB’s Davis said. “So this gap down in valuations gives some companies an opportunity to enter at a more attractive entry point.”

Healthcare technology companies, the majority of which have yet to become profitable, may be hit the hardest by lower valuations if they go to the market, according to Davis.

“I can't imagine a world where valuations stay at these levels,” Davis said. “It's like the pendulum swung in the other direction ... I'm starting to see extremely high quality names start to trade at head-scratching multiples.”

The downturn could lead to more companies conducting mergers of equals, which may make companies more robust and unlock more financing options, Norris added.

“But the problem there is, nobody likes to be the acquiree,” Norris said. “Everyone likes to be the acquirer.”

Correction: A previous version of this story incorrectly stated Definitive Healthcare was acquired.